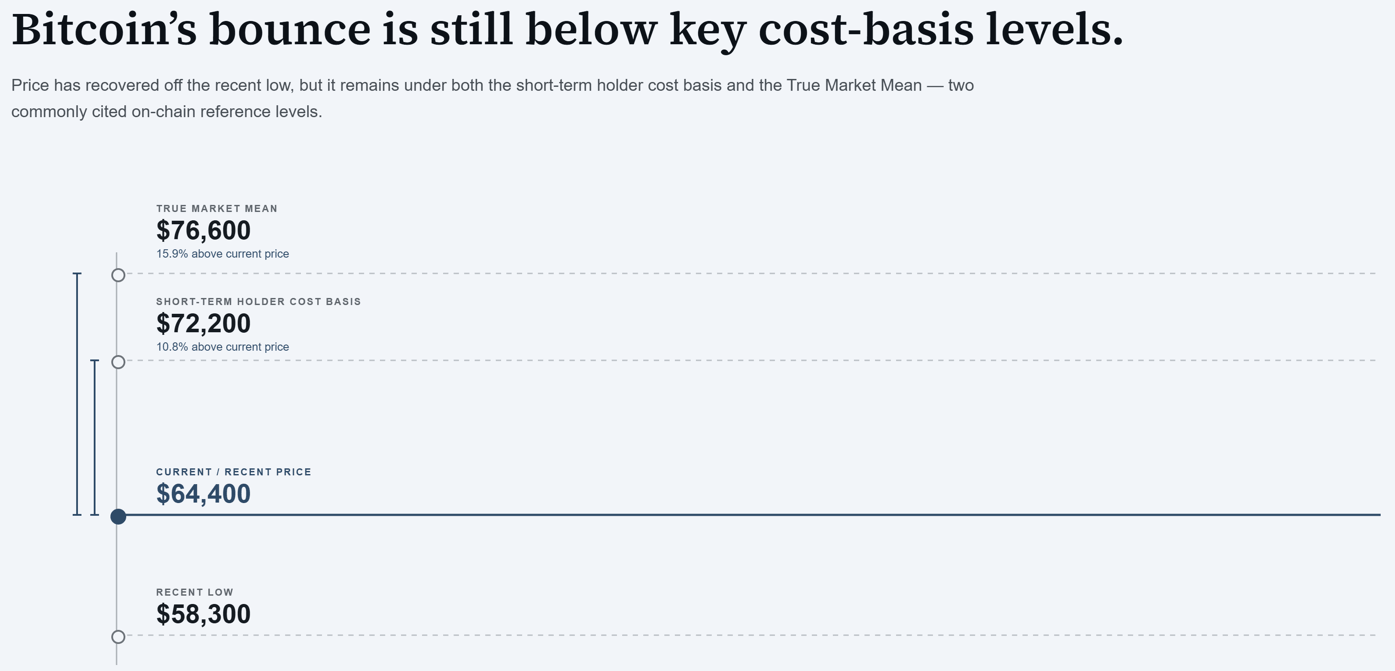

Bitcoin’s climb from $58,300 to $64,400, then back to $62,700, over the past week is a bounce that still leaves the price below two important levels tracked by Glassnode: the True Market Mean near $76,600 and the short-term holder cost basis near $72,200.

The firm places Bitcoin in the later stages of a bottoming process, which it frames as ongoing.

The Federal Reserve released the minutes from its June meeting on July 8, showing that all participants supported holding the federal funds target range at 3.50% to 3.75%, and the committee removed language from prior statements that had signaled a bias toward easing.

Glassnode’s on-chain data indicate a market working through the kind of exhaustion that typically precedes a bottom, and the Fed’s language suggests a policy environment still weighing whether inflation requires a firmer response.

Long-term holders are the signal to watch

Bitcoin trading below the True Market Mean matters because Glassnode treats that level as a cycle-wide cost-basis anchor. A sustained reclaim would point to broader repair than the current bounce has delivered.

Glassnode’s framing points to long-term holder loss realization, the pace at which holders who bought Bitcoin more than 155 days ago are selling at a loss.

That metric now accounts for 43% of total realized value on the network, up from 15% in early February, and recently peaked at nearly $280 million per day, the highest level since December 2022.

Glassnode says the current wave of long-term holder capitulation continues, and the market needs a meaningful compression in that number before it can credibly transition back toward bull market conditions.

Spot Bitcoin ETF net flows have improved from a low near $193 million per day in early June to a 30-day average near $88.9 million per day now, a real recovery that still leaves the market in a net-outflow regime.

Trading volume is running at a 30-day average of about $650 million to $950 million per day, far below the October 2025 peak near $4.4 billion.

A return to that peak would require roughly $3.45 billion to $3.75 billion per day in additional ETF turnover, a scale of activity current flows are nowhere close to producing.

The options market’s open-interest put/call ratio fell to 0.56, the lowest reading of 2026, while perpetual futures funding sits well below the 0.01% level Glassnode uses as a neutral benchmark, with both readings less bearish than the spot and ETF data.

The same options market still prices real downside protection, with a 25-delta skew that stays bid across maturities, meaning traders are paying up for puts relative to calls at every time frame Glassnode tracks.

| Signal | Current reading | What it means |

|---|---|---|

| Long-term holder losses | ~$280M/day peak | Capitulation remains elevated |

| LTH losses as share of realized value | 43% | Long-term holders are driving a large share of realized stress |

| ETF netflows | ~-$88.9M/day 30-day average | Outflows have eased but remain negative |

| ETF trading volume | $650M–$950M/day | Institutional activity remains far below peak |

| ETF volume gap vs Oct. 2025 peak | ~$3.45B–$3.75B/day | Return to peak demand would require a major volume recovery |

| Options put/call ratio | 0.56 | Less bearish positioning than spot/ETF data imply |

| Perpetual funding | Below 0.01% neutral level | Leverage demand remains muted |

| 25-delta skew | Puts bid across maturities | Traders still pay for downside protection |

What the Fed minutes said and what Bitcoin needs

The minutes describe participants seeing inflation running higher and staying well above the Fed’s 2% objective, pointing to tariffs, supply disruptions tied to the Strait of Hormuz, and AI-related demand as drivers, with many participants saying elevated commodity prices and supply disruptions could persist longer than officials had expected.

Most participants described a scenario where inflation pressures ease enough to hold rates steady or eventually cut them. They also discussed a second scenario in which inflation remains elevated due to AI demand, the Middle East conflict, or tariffs, and said that in that case, policy firming would be warranted.

In the case where investors’ capitulation cools first, long-term holder losses compress sharply toward $100 million to $150 million a day, ETF flows turn neutral to positive with volume climbing back above $1 billion a day, and incoming inflation data softens enough to take the Fed’s policy-firming scenario off the table.

Under that path, Bitcoin reclaims the short-term holder cost basis first, then works toward testing the True Market Mean itself.

In the case where the macro backdrop keeps sellers active, long-term holder losses remain near or above $250 million per day, ETF net flows remain negative, and Fed rhetoric keeps policy-firming risk alive through the next inflation prints.

Along that path, Bitcoin remains structurally vulnerable and could retest the lower end of its bear-market range near its realized price.

Using absolute values to frame market stress, Glassnode’s two pressure points, long-term holder losses near $280 million a day and ETF net outflows near $88.9 million a day, put the combined stress reading near $369 million a day.

| Condition | Bull path | Bear path |

|---|---|---|

| Long-term holder losses | Compress toward $100M–$150M/day | Stay near or above $250M/day |

| ETF netflows | Turn neutral to positive | Remain negative |

| ETF trading volume | Rises above $1B/day and keeps climbing | Stays below $1B/day |

| Fed backdrop | Inflation softens; policy-firming risk fades | Inflation risks keep firming scenario alive |

| First technical/on-chain reclaim | Short-term holder cost basis near $72.2K | Price remains below recent-buyer breakeven |

| Larger confirmation level | True Market Mean near $76.6K | Lower bear-market range remains in play |

| Article takeaway | Bottoming process starts confirming | Bottoming process stretches out |

Bitcoin’s bottoming process would start to look more credible if three conditions develop together: long-term holder losses compress, ETF outflows approach neutrality, and institutional volume climbs back toward the level it reached in October 2025.

The Fed’s June minutes gave the market fewer reasons to expect an easy path.

The post Bitcoin’s bottom needs long-term holders to stop losing $280M a day appeared first on Crypto Finders