Strategy made nearly $2 billion on Bitcoin this year but SEC filing hides a far bigger number

Strategy (formerly MicroStrategy) is claiming its aggressive Bitcoin purchases have yielded a nearly $2 billion gain this year despite the top asset’s clear price struggles.

However, a close look at the enterprise software company’s legally binding regulatory filings tells a much redder story: under standard accounting rules, the firm is nursing a multi-billion dollar unrealized loss, and its aggregate Bitcoin stack sits firmly underwater.

Despite the paper losses, the company shows no signs of slowing. Armed with a highly liquid capital markets engine, Strategy continues to issue equity to fund massive daily purchases, completely unfazed by the disconnect between its curated corporate dashboard and its sobering regulatory reality.

A bespoke winning streak

By its own metrics, Strategy’s Bitcoin treasury playbook is flawless despite the prevailing bear market situation in the broader crypto market.

On X, the company said its BTC purchasing strategy has generated nearly $1.7 billion in Bitcoin gains since January this year.

That metric caps off a historic accumulation streak that has fundamentally warped the crypto market’s supply dynamics.

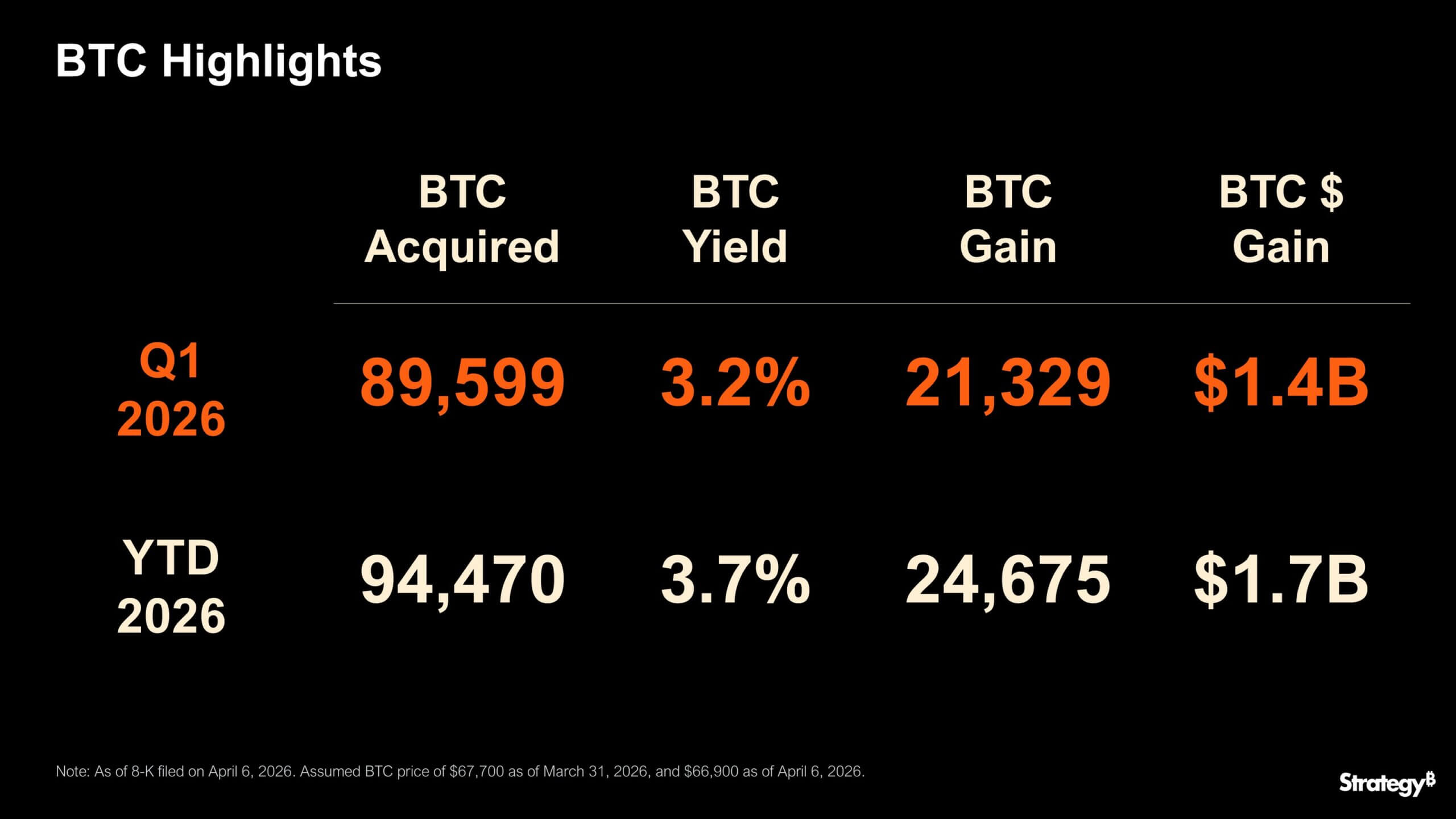

Notably, Strategy disclosed that it has acquired an astonishing 2.2 times the newly mined Bitcoin supply over the period. This equates to more than 94,000 BTC since the beginning of the year.

To quantify this, Strategy’s management points to two proprietary metrics: “BTC Yield” and “BTC Gain.” Strategy reports achieving a BTC Yield of 3.7% this year, generating a BTC Gain of 24,675 coins (roughly $1.7 billion).

For retail investors and crypto advocates, these figures are definitive proof that the company’s leveraged accumulation strategy is working.

Strategy’s Bitcoin gain metric is designed to reward balance-sheet expansion on a per-share basis. In its annual report, the company says BTC Yield measures the percentage change in Bitcoin Per Share (BPS) from the beginning to the end of a period.

BTC Gain then converts that percentage change into an absolute Bitcoin figure by multiplying the amount of Bitcoin held at the start of the period by BTC Yield. BTC $ Gain goes one step further by multiplying BTC Gain by the market price of Bitcoin.

The $14 billion SEC reality

However, the transition from the company’s marketing materials to its Securities and Exchange Commission filings, and the $1.7 billion gain, is eclipsed by a staggering accounting deficit.

Strategy’s quarter-end filing states the firm recorded a $14.46 billion unrealized loss on its digital assets for the three months ended March 31.

Under the fair-value accounting rules adopted in January 2025, market price fluctuations must flow directly through the income statement. Because Bitcoin’s price slipped between year-end and March 31, Strategy was forced to slash the official carrying value of its digital assets from $58.85 billion down to $51.65 billion.

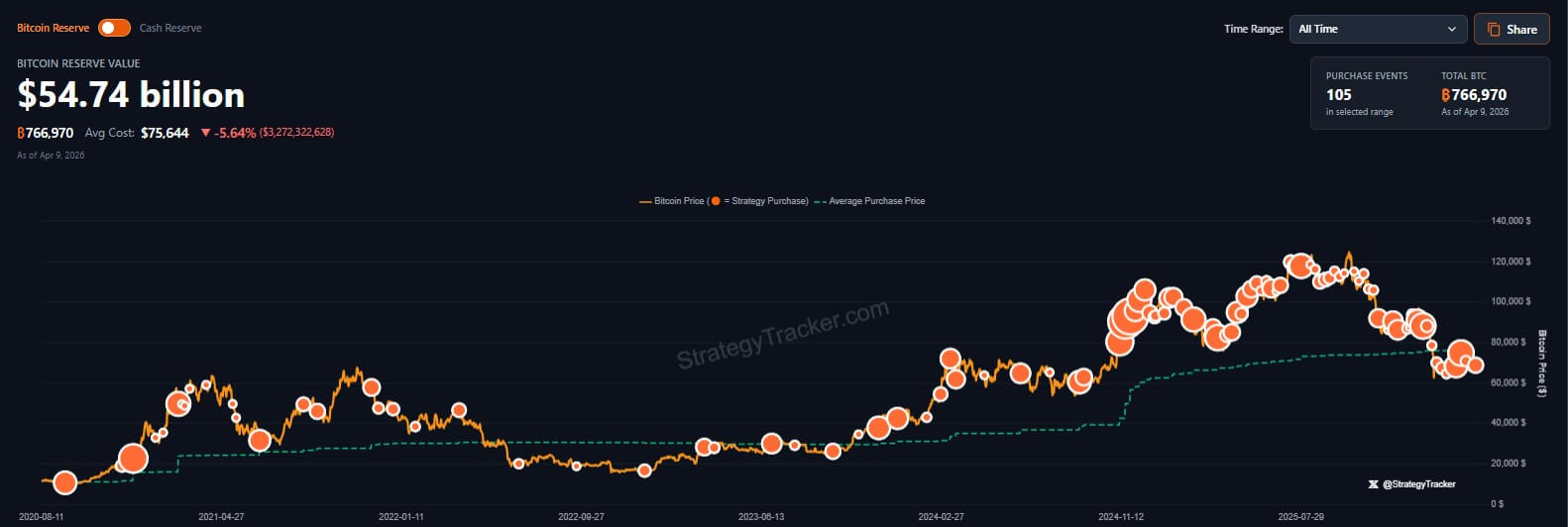

Beyond the quarter-end accounting losses, the company’s aggregate cost basis is also underwater. Strategy bought heavily into a weakening market through the first quarter, pushing its total holdings to 766,970 BTC. The total acquisition cost was $58.02 billion, averaging $75,644 per coin.

With Bitcoin currently trading near $71,192, that reserve is worth approximately $54.60 billion, placing the company roughly $3.41 billion below its aggregate cost.

Strategy’s Bitcoin buying continues with STRC

Despite billions in paper losses and an average purchase price that exceeds the open market value, Strategy insists it will not sell a single coin. Instead, it is doubling down.

The ultimate proof of the market’s willingness to fund this conviction lies in the company’s STRC preferred stock issuance.

STRC is a high-yield credit structure that pays an 11.5% annual dividend. The asset is designed to trade closely to its par value of $100, and Strategy can efficiently leverage its at-the-market (ATM) issuance program to fund aggressive Bitcoin acquisitions.

In fact, STRC.live estimates show that STRC saw its daily volume reach $333 million, the seventh-highest trading volume since launch, on April 8. This day’s trading could fund the purchase of more than 2,000 additional Bitcoins.

The numbers are a critical indicator of financial health for Strategy’s specific playbook, signaling that demand for the firm’s equity remains bottomless.

As long as Wall Street eagerly absorbs equity offerings at a stable valuation, Strategy faces no immediate pressure to halt its operations.

Where the pressure sits

The company’s own disclosures show why the dashboard metric and the ongoing buying streak do not settle the larger balance-sheet question.

Strategy acknowledges that its Bitcoin KPIs do not take into account existing and future liabilities, nor the preferential rights of preferred stockholders to dividends and assets in a liquidation scenario.

The annual report adds that purchases financed with non-convertible notes or preferred stock can simultaneously artificially lift BTC Yield, BTC Gain, and BTC $ Gain while also increasing overall indebtedness and senior claims on the asset pool.

That qualification has become increasingly important as the capital structure expands. Strategy said in February that it had established a $2.25 billion USD Reserve providing about 2.5 years of dividend and interest coverage.

However, STRC has scaled to a $3.4 billion market cap, and cumulative preferred distributions paid had reached $413 million at a blended annual rate of 9.6%.

Crucially, the annual report explicitly states that the software business is not expected to generate sufficient operating cash flow over the next 12 months to meet the company’s financial obligations and liquidity needs, meaning that continuous financing remains the lifeblood of the model.

This means that a significant decline in the market value of Strategy’s Bitcoin holdings, or a negative shift in investor sentiment and financing conditions, could impair the firm’s ability to raise enough equity or debt financing to meet obligations.

These risks are most likely to materialize when Bitcoin is trading below its carrying value or cost basis. If the company cannot secure financing in time or on acceptable terms, Strategy has conceded that it may be required to sell Bitcoin to satisfy financial obligations or liquidity needs.

For now, the machine is still running. Strategy is adding Bitcoin, the marketing dashboard still shows positive Bitcoin gain, and STRC remains anchored near par while supplying fresh capital.

The post Strategy made nearly $2 billion on Bitcoin this year but SEC filing hides a far bigger number appeared first on Crypto Finders