Este artículo también está disponible en español.

Zaheer Ebtikar, the Chief Investment Officer (CIO) and founder of Split Capital—a hedge fund specializing in liquid token investments—has attributed the Ethereum underperformance over the last months to strategic missteps by the Ethereum Foundation and structural shifts in crypto capital flows. In an analysis shared via X (formerly Twitter), Ebtikar writes, “Independent of the myriad of (probable) bad decisions that the ETH foundation & co have made there’s another structural reason why ETH has traded like a dog this cycle.”

Why Is The Ethereum Price Lagging Behind?

Ebtikar began by emphasizing the importance of understanding capital flows within the crypto market. He identified three primary sources of capital flow: retail investors who engage directly through platforms like Coinbase, Binance, and Bybit; private capital from liquid and venture funds; and institutional investors who invest directly through Exchange-Traded Funds (ETFs) and futures. However, he noted that retail investors are “hardest to quantify” and are “not fully present in the market today,” thus excluding them from his analysis.

Focusing on private capital, Ebtikar highlighted that in 2021, this segment was the largest capital base, driven by crypto euphoria that attracted more than $20 billion in net new inflows. “Fast forward to today, private capital is no longer the heavy hitter capital base as ETFs and other traditional vehicles have taken the role of the largest net new buyer of crypto,” he stated. He attributed this decline to a series of poor venture investments and overhang from prior cycles, which have “left a bad taste in the mouths of LPs.”

These venture firms and liquid funds recognized that they couldn’t wait out another cycle and needed to be more proactive. They began taking more “shots on target” for liquid plays, often through private deals involving locked tokens such as Solana (SOL), Celestia (TIA), and Toncoin (TON). “These locked deals also represented something more interesting for a lot of firms—there’s a world outside of Ethereum-based investing that is actually growing and usable and has enough market cap growth relative to ETH that could justify the underwriting of the investment,” Ebtikar explained.

Related Reading

He noted that investors were aware it would be increasingly difficult to raise funds for venture and liquid investments. Without the return of retail capital, institutional products became the only viable avenue for a bid for ETH. Mindshare began fragmenting as the three-year mark of the 2021 vintage approached, and products like BlackRock’s spot Bitcoin ETF (IBIT) gained legitimacy as the de facto benchmark for crypto. Private capital had to make a choice: “Abandon their core portfolio hold in ETH and move down the risk curve or hold your breath for traditional players to start bailing you out.”

This led to the formation of two camps. The first consisted of pre-ETF ETH sellers between January and May 2024, who opted out of ETH and swapped to assets like SOL. The second group, post-ETF ETH sellers from June to September 2024, realized that ETF flows into ETH were lackluster and that it would take much more for ETH’s price to gain support. “They understood that the ETF flows were lackluster and it would take a lot more for ETH price to begin being supportive,” Ebtikar noted.

Turning his attention to institutional capital, Ebtikar observed that when spot Bitcoin ETFs like IBIT, FBTC, ARKB, and BITW entered the market, they exceeded expectations. “These products broke any realistic target investors and experts could’ve fathomed with their success,” he stated. He emphasized that Bitcoin ETFs have become some of the most successful ETF products in history. “BTC went from being a dog in the average portfolio to now the only funnel for net new capital in crypto and at a record rate too,” he said.

Despite Bitcoin’s surge, the rest of the market didn’t keep up. Ebtikar questioned why this was the case, pointing out that crypto-native investors, retail, and private capital had long since reduced their Bitcoin holdings. Instead, they were “stuck in altcoins and Ethereum as the core of their portfolio.” Consequently, when Bitcoin received its institutional bid, few in the crypto space benefited from the new wealth effect. “Few in crypto were beneficiaries of the newly made wealth effect,” he remarked.

Investors began to reassess their portfolios, struggling to decide their next moves. Historically, crypto capital would cycle from index assets like Bitcoin to Ethereum and then down the risk curve to altcoins. However, traders speculated on potential flows into Ethereum and similar assets but were “broadly wrong.” The market started to diverge, and the dispersion between asset returns intensified. Professional crypto investors and traders moved aggressively down the risk curve, and funds followed suit to generate returns.

Related Reading

The asset they chose to reduce exposure to was Ethereum—the largest asset in their core portfolios. “Slowly but surely ETH started losing steam to SOL and similar, and a non-trivial percentage of this flow started really moving downstream to memecoins,” Ebtikar observed. “ETH lost its moat in crypto-savvy investors, the only group of investors who were historically interested in buying.”

Even with the introduction of spot ETH ETFs, institutional capital paid little attention to Ethereum. Ebtikar described Ethereum’s predicament as suffering from “middle-child syndrome.” He elaborated, “The asset is not in vogue with institutional investors, the asset lost favor in crypto private capital circles, and retail is nowhere to be seen bidding anything at this size.” He emphasized that Ethereum is too large for native capital to support while other index assets like SOL and large caps like TIA, TAO, and SUI are capturing investor attention.

According to Ebtikar, the only way forward is to expand the universe of potentially interested investors, which can only happen at the institutional level. “ETH’s best odds of making a material comeback (short of changes to the core protocol’s trajectory) is to have institutional investors pick up the asset in the coming months,” he suggested. He acknowledged that while Ethereum faces significant challenges, it is “the only other asset with an ETF and likely will be for some time.” This unique position offers a potential avenue for recovery.

Ebtikar mentioned several factors that could influence Ethereum’s future trajectory. He cited the possibility of a Trump presidency, which could bring changes to regulatory frameworks affecting cryptocurrency. He also pointed to potential shifts in the Ethereum Foundation’s direction and core focus, suggesting that strategic changes could reinvigorate investor interest. Additionally, he highlighted the importance of marketing the ETH ETF by traditional asset managers to attract institutional capital.

“Considering the possibility of a Trump Presidency, change at the Ethereum Foundation’s direction and core focus, and marketing of the ETH ETF by traditional asset managers, there are quite a few outs for the father of smart contracting platforms,” Ebtikar remarked. He expressed cautious optimism, stating that not all hope is lost for Ethereum.

Looking ahead to 2025, Ebtikar believes it will be a critical year for cryptocurrency and especially for Ethereum. “2025 will very much be an interesting year for crypto and especially for Ethereum as so much of the damage from 2024 can be unwound or further deepened,” he concluded. “Time will tell.”

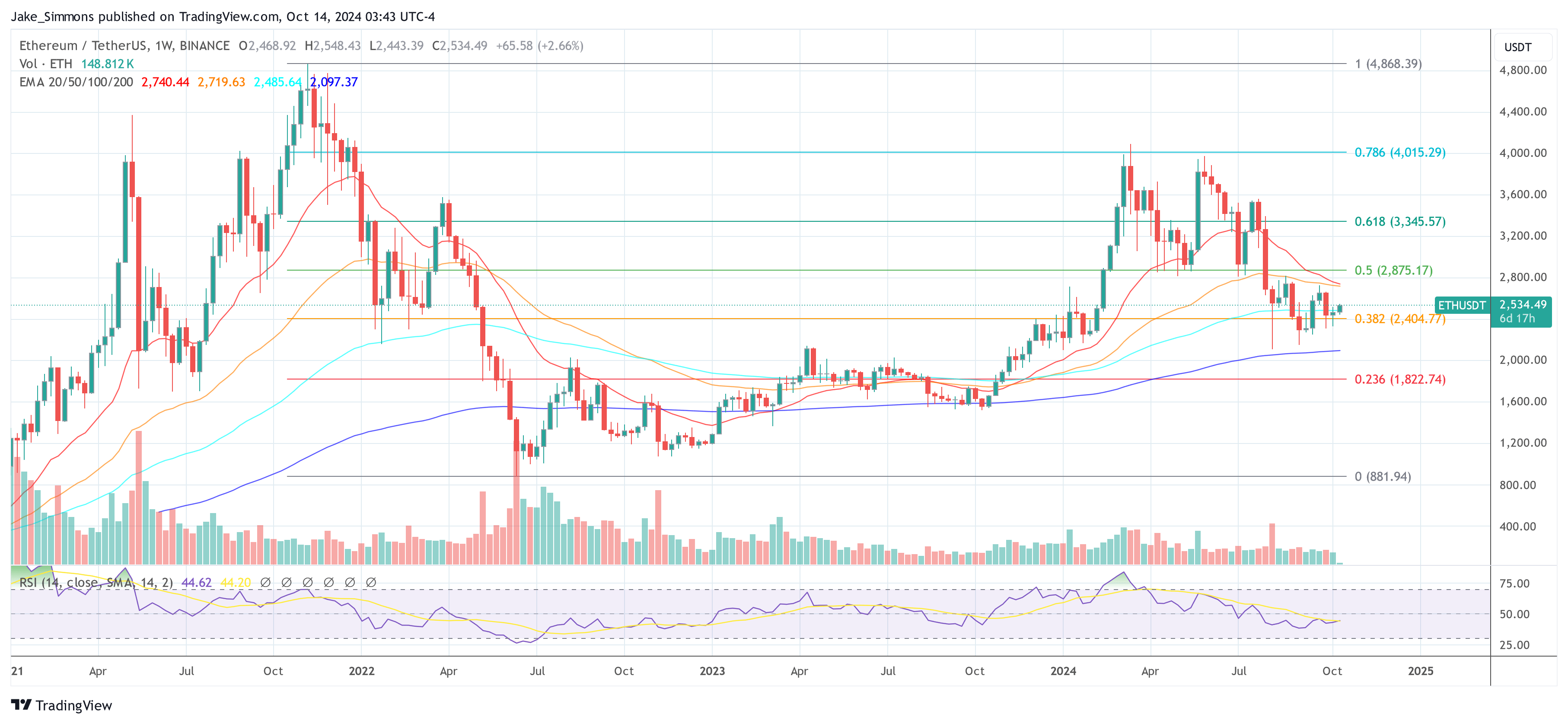

At press time, ETH traded at $2,534.

Featured image created with DALL.E, chart from TradingView.com