Bitcoin miners spent years racing to secure cheap electricity, and that electricity has since become more valuable than the Bitcoin mining business built on it.

That inversion drives Fidelity’s May 2026 assessment that AI hosting could give miners a second revenue stream while flattening Bitcoin’s hash rate as major operators redirect energy infrastructure away from pure mining, and two hyperscaler contracts have put a concrete price on what miners built.

Cipher Mining’s SEC-filed business update announced a roughly $5.5 billion, 15-year lease with AWS to provide 300 MW of turnkey space and power for AI workloads, with delivery beginning in July 2026.

IREN signed a roughly $9.7 billion, five-year GPU cloud contract with Microsoft, deploying NVIDIA GB300 GPUs through 2026 at its 750 MW Childress, Texas campus and supporting 200 MW of critical IT load.

| Miner | Hyperscaler | Contract value | Duration | Power / capacity | Delivery timeline | Why it matters |

|---|---|---|---|---|---|---|

| Cipher Mining | AWS | ~$5.5B | 15 years | 300 MW | Begins July 2026 | Shows powered mining sites can be leased as AI infrastructure |

| IREN | Microsoft | ~$9.7B | 5 years | 200 MW critical IT load at 750 MW Childress campus | GPUs deployed through 2026 | Shows miners can monetize power campuses through GPU cloud, not just BTC mining |

Miners had already secured land, grid interconnection, substations, and power rights, which are what AI data centers need and cannot build fast enough.

The 2024 halving compressed hash prices and pushed CoinShares’ tracked weighted-average cash cost to roughly $79,995 per BTC by the first quarter of 2026, prodding operators toward AI hosting as a revenue stabilizer, leasing unused capacity, keeping the mining rigs running, and offsetting the worst of the Bitcoin downturns.

CoinShares estimates public miners’ AI and HPC contracts had surpassed $70 billion in aggregate by early 2026, with listed miners on pace to derive as much as 70% of revenue from AI by year-end, up from roughly 30%.

That is a revenue hedge that the Cipher and IREN contracts have since displaced with price discovery for power campuses.

Price discovery changes the internal math

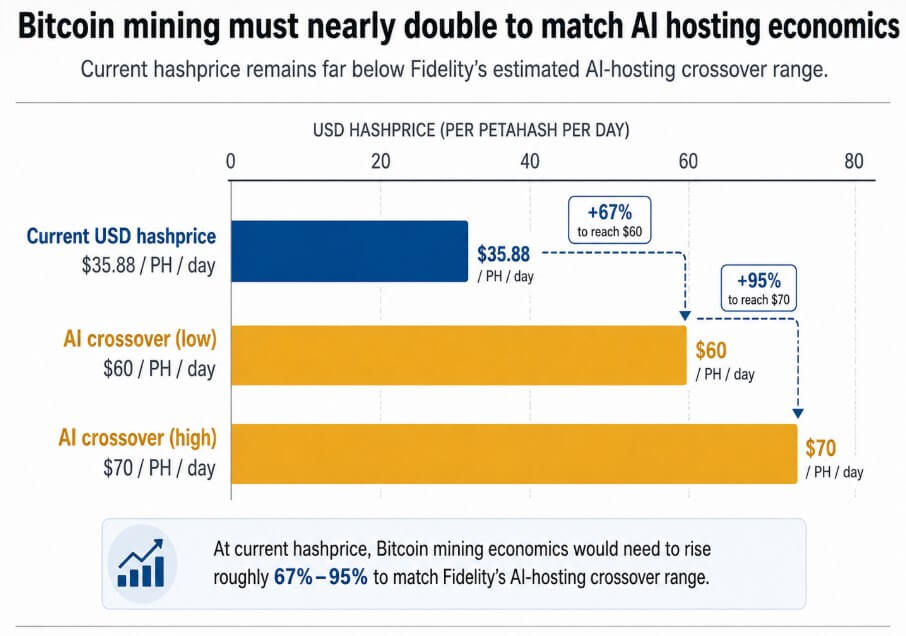

Fidelity’s January 2026 analysis identified a mining-to-AI crossover at roughly $60 to $70 per petahash per day for a 20-joule-per-terahash fleet, meaning most 20-to-25 J/TH miners would need the hash price to rise 40% to 60% to match contracted GPU-hosting economics.

The Hashrate Index’s May 25 data has since extended this distance, with the US dollar-denominated hash price at $35.88 per PH/day, placing the AI crossover at approximately 67% to 95% above the current spot.

A miner sitting on 300 MW of powered, permitted infrastructure now faces a choice between deploying ASICs and earning $35.88 per PH/day, or signing a hyperscaler lease at contracted rates that require hash price to nearly double to match.

AWS and Microsoft have effectively published a floor on what that infrastructure is worth to someone other than Bitcoin, and every major operator with comparable assets now has that number in their model.

AI infrastructure costs between $8 million and $15 million per megawatt to build, compared to $700,000 to $1 million for Bitcoin mining infrastructure, and miners who transition enter a more capital-intensive business with fundamentally different debt profiles, valuation metrics, and execution risk.

Hash rate may no longer follow BTC price alone

Bitcoin’s mining expansion historically followed price, with miners ordering more machines when BTC rose and cutting capacity when it fell.

VanEck’s April ChainCheck recorded 30-day hash rate momentum at the 16th percentile and 90-day momentum at the 9th percentile, the densest cluster of sustained hash-rate drawdowns since China’s 2021 mining ban.

CoinWarz data as of May 28 showed Bitcoin difficulty at 136.61T and a 90-day difficulty change of -5.40%, consistent with Fidelity’s picture of mining churn.

Bitcoin’s 2,016-block difficulty adjustment is still the counterweight, since every time hash rate exits, it lowers the computational cost of producing valid blocks and raises revenue per unit of remaining hash once difficulty resets.

A 20% hash-rate exit would lift surviving miners’ hash price to roughly $44.85 per PH/day, while a 30% exit would bring it to roughly $51.26, still well short of Fidelity’s AI crossover unless BTC price or transaction fees rise meaningfully.

Power locked into 15-year AWS leases or five-year Microsoft GPU contracts cannot rotate back to mining even if ASIC economics recover. In older cycles, idle hash returned because machines could be switched back on, while in this cycle the campuses themselves may be committed elsewhere.

Bitcoin gets the tighter market it needs

If BTC moves toward $100,000 to $140,000 or transaction fees rise materially, the economics realign.

A 20% reduction in network hash rate lowers the BTC price required to reach the $60 to $70 AI crossover to approximately $98,000 to $114,000, and a 30% reduction lowers that threshold to roughly $86,000 to $100,000.

Miners who are still committed to Bitcoin benefit from a market where hash price rises faster than hash rate, compressing the competitive field and improving margins for operators with efficient fleets and lower power costs.

Fewer large public miners in the hash rate mix also reduces the forced BTC selling that has historically pressured spot price during expansion cycles.

Charles Schwab’s May 26 analysis argues that hybrid infrastructure models strengthen Bitcoin’s overall network health: lower forced selling, tighter difficulty conditions, and better miner margins reduce the systemic stress that large capital-intensive miners have historically introduced at cycle peaks.

The industry separates into two distinct businesses, consisting of companies that own power campuses and monetize them through hyperscaler contracts, and companies that actually mine Bitcoin, often at lower-cost, more flexible, or stranded-energy sites where AI data centers cannot easily operate.

| Scenario | Hash-rate exit | Implied hashprice after difficulty reset | BTC price needed for $60/PH/day | BTC price needed for $70/PH/day | Takeaway |

|---|---|---|---|---|---|

| Status quo | 0% | $35.88 | ~$122K | ~$142K | Mining remains far below AI crossover |

| Moderate exit | 20% | ~$44.85 | ~$98K | ~$114K | Difficulty reset helps miners but does not fully close the gap |

| Larger exit | 30% | ~$51.26 | ~$86K | ~$100K | Bitcoin mining becomes more competitive if BTC rises or fees improve |

AI wins the allocation decision

If BTC holds below $70,000 to $80,000, fees stay thin, and power prices stay elevated, contracted GPU-hosting economics dominate internal capital allocation for operators with AI-ready sites.

CoinShares estimates that at roughly $30 per PH/day, between 15% and 20% of the global fleet becomes uneconomic if power costs $0.06 per kilowatt-hour or higher for machines with S19 XP efficiency or lower.

Older fleets shut down, difficulty declines across successive epochs, and surviving miners earn more per petahash, but not enough to close the gap with the Cipher and IREN contracts for operators who still have that choice.

The difficulty adjustment keeps the network running through any exit, and mining’s center of gravity moves as large public miners with AI-ready infrastructure become data-center landlords, while Bitcoin hash rate concentrates among operators with cheaper, more intermittent, or internationally diversified energy.

The IREN/Microsoft contract carries an explicit delivery-timeline clause that Reuters reported could trigger termination if milestones are missed, and miners carrying heavy debt alongside delayed AI revenue face an equity repricing from a Bitcoin proxy to an execution-risk asset.

The split is the outcome

The contest between ASICs and GPUs for miner capital plays out site by site, operator by operator, contingent on power contracts already signed and BTC price at the next halving.

Bitcoin’s network absorbs hash-rate exits through lower difficulty, and higher BTC price or fees can pull economics back toward mining for any operator who has not already committed power elsewhere.

The more durable consequence of the AWS and Microsoft deals is that they have made it possible to run a large, credibly profitable infrastructure business on the same sites that Bitcoin mining built, without mining a single block.

Whether that possibility becomes the default for the next generation of power-campus construction depends on where BTC price settles relative to $35.88, and how many more hyperscalers arrive with 15-year checkbooks before the next halving forces the question again.