Quantum computing has long served as Bitcoin’s most cinematic threat. It has the right ingredients for a high-drama warning, strange machines, broken cryptography, and the possibility of a future rewrite of digital trust.

Yet the greater danger facing Bitcoin today looks far more ordinary and far more commercial. It is artificial intelligence, and the pressure point is electricity.

That pressure is already visible. As of today, Bitcoin is trading at $77,845 on CryptoSlate, up 5% over 24 hours, 6.7% over seven days, and 9.2% over 30 days.

Price has recovered over the past month, but the mining side of the network is still operating under tighter economics than the market’s casual surface suggests.

In its Q1 2026 mining report, CoinShares said the weighted average cash cost to produce one Bitcoin among publicly listed miners rose to about $79,995 in Q4 2025. The same report said the current hashprice around $30 per petahash per day leaves an estimated 15% to 20% of the global fleet underwater if power costs are high enough.

That is where AI enters the picture with a much sharper edge than quantum. Quantum remains a serious long-term cryptographic issue. NIST has already finalized its first post-quantum standards because the migration clock is real, and IBM’s roadmap targets the first large-scale fault-tolerant quantum computer by 2029.

Those milestones deserve attention. They also describe a technology path that still has to arrive.

AI is already bidding for the same powered campuses, the same substations, the same fiber routes, and the same land positions that gave industrial Bitcoin miners their strategic value in the first place.

One threat sits on the roadmap. The other is already signing leases, funding conversions, and changing how these companies use their best assets.

AI is already taking the premium sites

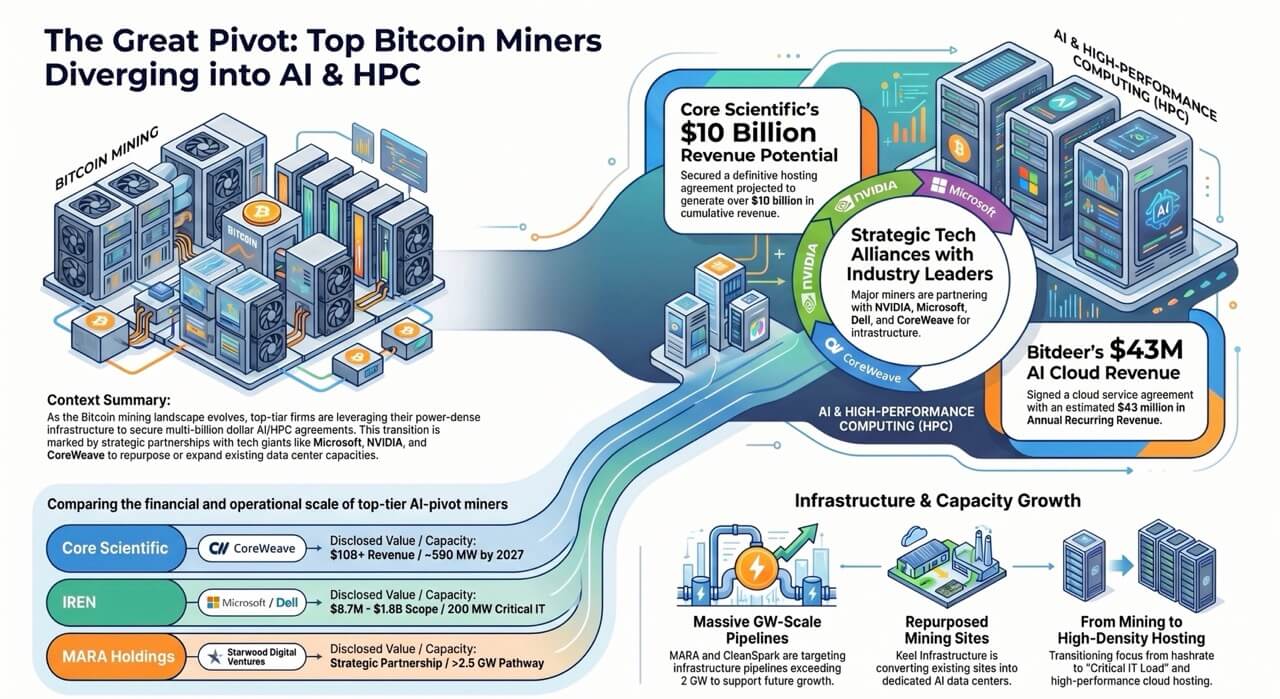

The strongest evidence comes from what miners are physically doing with their facilities. In March, Bitdeer said decommissioning of Bitcoin mining rigs had begun at its Tydal, Norway site to make room for a new AI data center.

That carries more weight than a lot of future doom posts about “Q-Day“. A miner with deep roots in Bitcoin chose to remove rigs from a live mining site because the economics of AI infrastructure made better use of the space.

Bitdeer also disclosed roughly $21 million in annual recurring revenue from external GPU cloud subscriptions as of Feb. 28, with negotiations ongoing with additional colocation tenants. The move was concrete, and it had already begun.

Riot has reached a similar conclusion from another angle. In its full-year 2025 results, Riot said its data center lease with AMD became operational and had been generating revenue since January 2026.

The company has also been clear that Rockdale can evolve into a much larger data center campus over time.

Core Scientific is even further down that road. In its fourth-quarter 2025 results, the company said around 350 MW had already been energized under its CoreWeave contract and that it remains on track to deliver around 590 MW by early 2027.

MARA’s partnership with Starwood was equally revealing in a different way, because it described campuses designed to operate both Bitcoin mining and AI compute, with the ability to toggle workloads depending on pricing and customer demand.

The pattern extends well beyond one company. According to the current public miner hashrate ranking, the top public miners by operating scale include Bitdeer at 69.5 EH/s, MARA at 61.7 EH/s, CleanSpark at 47.3 EH/s, IREN at 43 EH/s, and Riot at 36.4 EH/s.

This is a meaningful slice of the industrial Bitcoin mining landscape, and it is already splitting into three camps. Some miners have signed real AI or HPC contracts and are moving capacity. Some have frameworks and early pilots. Some are still largely tied to Bitcoin.

CoinShares estimates that more than $70 billion in cumulative AI and HPC contracts have now been announced across the public mining sector, and that listed miners could derive as much as 70% of revenue from AI by the end of this year, up from roughly 30% today.

| Rank | Miner | Current EH/s | Planned EH/s | AI / HPC | Status |

|---|---|---|---|---|---|

| 1 | Bitdeer (NASDAQ: BTDR) | 69.50 | 8.60 | AI Cloud ARR about $43M; Tydal Norway AI colocation buildout; tenant value undisclosed | In buildout |

| 2 | MARA Holdings (NASDAQ: MARA) | 61.70 | n/a | Starwood Digital Ventures; AI infrastructure platform; 1 GW near-term capacity; value undisclosed | Framework |

| 3 | CleanSpark (NASDAQ: CLSK) | 47.30 | 2.70 | Submer framework for AI and HPC campuses; no disclosed contract value | Framework |

| 4 | IREN (NASDAQ: IREN) | 43.00 | 3.00 | Microsoft AI cloud agreement about $9.7B; Dell hardware purchases about $5.8B | Signed |

| 5 | Riot Platforms (NASDAQ: RIOT) | 36.40 | 6.10 | AMD lease and services agreement; about $311M base value; up to about $1B with extensions | Signed |

| 6 | Cango (NYSE: CANG) | 27.98 | 9.03 | DL Holdings financing for EcoHash AI and HPC; $65M investment plus $10M note | Signed financing |

| 7 | HIVE Digital (NASDAQ: HIVE) | 22.20 | 3.30 | BUZZ HPC signed AI cloud contracts; about $30M total contract value over two years | Signed |

| 8 | American Bitcoin (private) | 21.90 | 6.20 | No disclosed AI or HPC agreement | None disclosed |

| 9 | Core Scientific (NASDAQ: CORZ) | 15.70 | 2.20 | CoreWeave hosting agreements; over $10B potential cumulative revenue | Signed |

| 10 | Keel Infrastructure | 14.80 | n/a | Washington AI and HPC site conversion; binding $128M agreement | Binding |

This reversal now shapes the sector. The public companies once pitched as leveraged bets on Bitcoin increasingly look like owners of scarce power infrastructure that can be rented to a richer customer base.

That shift does not require anyone to stop believing in Bitcoin. It only requires a board to compare the cash flow from mining against the cash flow from leasing out premium power and compute space. Fiduciary duty does the rest.

The danger for Bitcoin is immediate

At an average Bitcoin price of around $80,000, the revenue picture still skews toward mining at the sector level.

Using the current hashrate distribution for the top 10 public miners and allocating annual block rewards in proportion to operating hash, the group still throws off a larger Bitcoin revenue pool than the AI contract base currently visible across the same cohort.

That leaves Bitcoin in front on aggregate revenue even after the sector’s high-profile move into AI and HPC.

The balance changes once the comparison shifts from the whole group to the companies with the strongest signed infrastructure deals, because a small number of names already have AI economics that can rival or exceed what their Bitcoin fleets are likely to generate at this price level.

| Company | Current Hashrate (EH/s) | Estimated BTC Mined / Year | BTC Revenue at $80,000 | BTC Revenue at $160,000 |

|---|---|---|---|---|

| Bitdeer | 69.50 | 11,210.2 | $896.8M | $1.794B |

| MARA | 61.70 | 9,952.1 | $796.2M | $1.592B |

| CleanSpark | 47.30 | 7,629.4 | $610.3M | $1.221B |

| IREN | 43.00 | 6,935.8 | $554.9M | $1.110B |

| Riot | 36.40 | 5,871.2 | $469.7M | $939.4M |

| Cango | 27.98 | 4,513.1 | $361.0M | $722.1M |

| HIVE | 22.20 | 3,580.8 | $286.5M | $572.9M |

| American Bitcoin | 21.90 | 3,532.4 | $282.6M | $565.2M |

| Core Scientific | 15.70 | 2,532.4 | $202.6M | $405.2M |

| Keel Infrastructure | 14.80 | 2,387.2 | $191.0M | $382.0M |

| Total | 360.48 | 58,144.5 | $4.652B | $9.303B |

That split is the important part. The sector is no longer moving in one direction at one speed. For miners without a large contracted AI revenue stream, Bitcoin still looks like the main engine of top-line performance if price holds around current levels.

For the subset that has already locked in major AI leases or cloud agreements, the income mix starts to look very different.

The result is a two-track market. One track still depends primarily on Bitcoin’s price and network economics. The other increasingly depends on whether a miner controls premium power sites that can be turned into long-duration compute revenue.

| Company | Confirmed Annual AI Revenue | If Contract Value Doubled |

|---|---|---|

| Bitdeer | $21.0M | $42.0M |

| MARA | $0 | $0 |

| CleanSpark | $0 | $0 |

| IREN | N/A from disclosed annual run-rate | N/A |

| Riot | $31.1M | $62.2M |

| Cango | $0 | $0 |

| HIVE | $15.0M | $30.0M |

| American Bitcoin | $0 | $0 |

| Core Scientific | N/A from disclosed annual run-rate | N/A |

| Keel Infrastructure | N/A from disclosed annual run-rate | N/A |

| Total | $67.1M | $134.2M |

The comparison becomes even sharper when Bitcoin is modeled at $160,000. At that level, mining revenue expands fast enough that the top 10 group’s Bitcoin business pulls well clear of the current AI contract base, even when the larger signed AI agreements are annualized for comparison. That does not erase the attraction of AI.

It changes the relative urgency of the pivot. A stronger Bitcoin price gives miners more room to keep their best sites pointed at hashing and still justify the opportunity cost. It also raises the bar AI has to clear before boards feel pressure to repurpose prime campuses away from Bitcoin.

| Scenario | Annual Revenue |

|---|---|

| Bitcoin Revenue, BTC at $80,000 | $4.652B |

| Bitcoin Revenue, BTC at $160,000 | $9.303B |

| AI Revenue, Confirmed Annual Run-Rate | $67.1M |

| AI Revenue, Confirmed Contracts Doubled | $134.2M |

| AI Revenue, 10-Year Sensitivity | $2.070B |

| AI Revenue, 10-Year Sensitivity if Doubled | $4.140B |

The more revealing sensitivity test comes from doubling the AI contract base.

Under that scenario, annual AI revenue moves much closer to what the group could make from mining at an $80,000 Bitcoin price. That is the zone where the business model starts to look genuinely contested.

Bitcoin still holds the larger aggregate pool in the base case, but the gap narrows as site quality, contract duration, financing terms, and execution start carrying more weight than ideology. Once that happens, the debate stops being about whether miners “believe” in Bitcoin and shifts toward which use of power produces the better return over the next several years.

That is also where the company-level results matter more than the sector average. The aggregate numbers still show Bitcoin with the stronger hand, especially in a higher-price environment.

The company-level numbers show something else: a small group of miners already has AI revenue potential that can outrun mining revenue at today’s Bitcoin price assumptions. Those are the names that make the broader threat credible.

They show that AI does not need to displace the whole mining industry to reshape it. It only needs to pull enough premium capacity away from Bitcoin to change who mines, where mining happens, and how much of the public miner complex still behaves like a direct proxy for Bitcoin itself.

Taken together, the revenue math supports a more precise conclusion than either extreme allows.

Bitcoin mining still offers the larger top-line opportunity for the top 10 group in aggregate, and that advantage widens further if Bitcoin enters a materially higher price regime.

AI still has a powerful claim on the best campuses because the economics are already superior for a subset of operators, and that advantage grows quickly if contract values continue to expand.

The likely result is a hybrid sector rather than a clean break, with some miners staying Bitcoin-first and others becoming power-and-compute businesses that treat Bitcoin as a secondary workload.

| Company | AI Annual Revenue, 10-Year Sensitivity | If Contract Value Doubled |

|---|---|---|

| Bitdeer | $21.0M | $42.0M |

| MARA | $0 | $0 |

| CleanSpark | $0 | $0 |

| IREN | $970.0M | $1.940B |

| Riot | $31.1M | $62.2M |

| Cango | $0 | $0 |

| HIVE | $15.0M | $30.0M |

| American Bitcoin | $0 | $0 |

| Core Scientific | $1.020B | $2.040B |

| Keel Infrastructure | $12.8M | $25.6M |

| Total | $2.070B | $4.140B |

Why AI reaches Bitcoin’s security budget first

The clearest way to understand the comparison is to separate engineering risk from economic risk. Quantum is an engineering risk to cryptography. AI is an economic risk to Bitcoin’s industrial security base.

One points toward a future need to upgrade signature schemes and harden the protocol over time. The other is already changing where capital goes, where machines are deployed, and which activities deserve the best power on the grid.

That makes AI the more immediate pressure point for Bitcoin’s security budget. Bitcoin stays secure because miners spend real money to produce hash and defend block production under known attack assumptions.

Difficulty adjustment keeps blocks coming, yet it does not erase the underlying economics. A network whose best-connected industrial operators increasingly treat Bitcoin as the lower-value use case for premium campuses faces a slower and more practical problem.

The security layer can continue to function while the best sites, the best interconnection rights, and the most financeable infrastructure migrate toward AI tenants.

Over time, that pushes Bitcoin mining toward cheaper, more interruptible, and often lower-quality power. CoinShares says exactly that in its sector review, arguing that AI is likely to drive Bitcoin mining toward more intermittent and cheaper power sources over the long term.

The scale of outside demand helps explain why. In its Energy and AI outlook, the International Energy Agency said global electricity consumption for data centers is projected to roughly double to around 945 TWh by 2030 in its base case.

That is a vast increase in power demand, making it even harder to assemble sites that are already difficult to assemble. Land, interconnection, permits, cooling design, and transmission access all take time. Bitcoin miners spent years collecting exactly those ingredients.

AI now wants them too, and AI customers often bring longer contracts, larger balance sheets, and smoother revenue visibility than mining can provide in a post-halving environment.

Quantum lacks that near-term commercial pull on the Bitcoin mining fleet. It may one day force a protocol transition and a broad wallet migration, and that prospect is serious.

Yet quantum does not currently offer miners a higher-return alternative for the same substation. AI does.

Quantum does not show up today as a tenant willing to sign for hundreds of megawatts of critical IT load. AI does.

Quantum does not produce a board-level argument for removing miners from a live site this quarter. AI already has.

How the next decade could reshape miners and the network

A full exodus from Bitcoin remains the low-probability extreme, because the network adapts and because many miners will keep one foot in both worlds for as long as the numbers justify it.

The more realistic path is a prolonged sorting process where premium, always-on campuses drift toward AI, while Bitcoin mining concentrates in flexible-power environments where interruption is acceptable, and site economics are harder for hyperscale AI tenants to use.

That outcome still changes Bitcoin in important ways.

First, public miner equities become less direct proxies for Bitcoin itself. Investors buying listed miners have often treated them as amplified expressions of the Bitcoin cycle. That relationship weakens as a larger share of enterprise value comes from data center leasing, power monetization, and AI execution risk.

Second, the composition of Bitcoin’s industrial hash shifts. Public miners may still mine significant amounts of Bitcoin, but more of the marginal security spend could come from operators with cheaper power, smaller footprints, or lower-cost geographies.

Third, treasury behavior may change. When companies are funding campus conversions, cooling systems, and higher-density compute buildouts, Bitcoin on the balance sheet starts looking more like a funding source than a sacred reserve. Riot’s earlier decision to sell Bitcoin to finance the Rockdale land purchase offered a clear preview of that logic.

The biggest live variable is still Bitcoin price. A return toward Bitcoin’s previous all-time high near $126,000 could lift hashprice toward $59 per petahash per day. A move like that would improve mining economics and slow the urgency of the pivot.

Yet even that would not erase the structural shift underway.

AI demand is feeding on a global infrastructure buildout that extends far beyond crypto. The IEA’s demand curve, the large signed contracts already on miner balance sheets, and the physical repurposing of real campuses all point in the same direction.

Over the next decade, the question may no longer be whether miners leave Bitcoin entirely. The sharper question is which parts of the mining stack remain worth dedicating to Bitcoin once AI is willing to pay more for the best land, the best power, and the best grid positions.

Quantum still belongs on Bitcoin’s list of strategic risks.

AI belongs on the list of operational and financial risks right now.

One threatens the code if the technology arrives at scale. The other is already competing for the machines, the megawatts, and the people who keep the network secure.

For the next several years, that is the threat with the more direct line into Bitcoin’s security budget, and it is already rewriting the miner business model in plain sight.